The Anchoring Effect- How an Income Floor Changes Your Entire Portfolio’s Behavior

By Dora Wysocki, CAS

When building a retirement or long-term investment portfolio, most conversations revolve around asset allocation. You’ve likely heard the classic debate: How much should you put into stocks versus bonds? But focusing strictly on the traditional stock-and-bond mix misses a powerful psychological and financial mechanism: the income floor.

An income floor is a stream of guaranteed, contractual income that covers your essential living expenses. This isn’t just a safety net; it’s a strategic anchor. By securing a reliable base of income, you fundamentally alter how the rest of your volatile assets behave—and how you behave as an investor.

Here is how a contractual income base stabilizes a portfolio and unlocks greater financial flexibility.

1. De-risking the Sequencing of Returns

The greatest threat to a newly retired portfolio isn’t a market crash; it’s a market crash combined with forced withdrawals. This is known as sequence of returns risk.

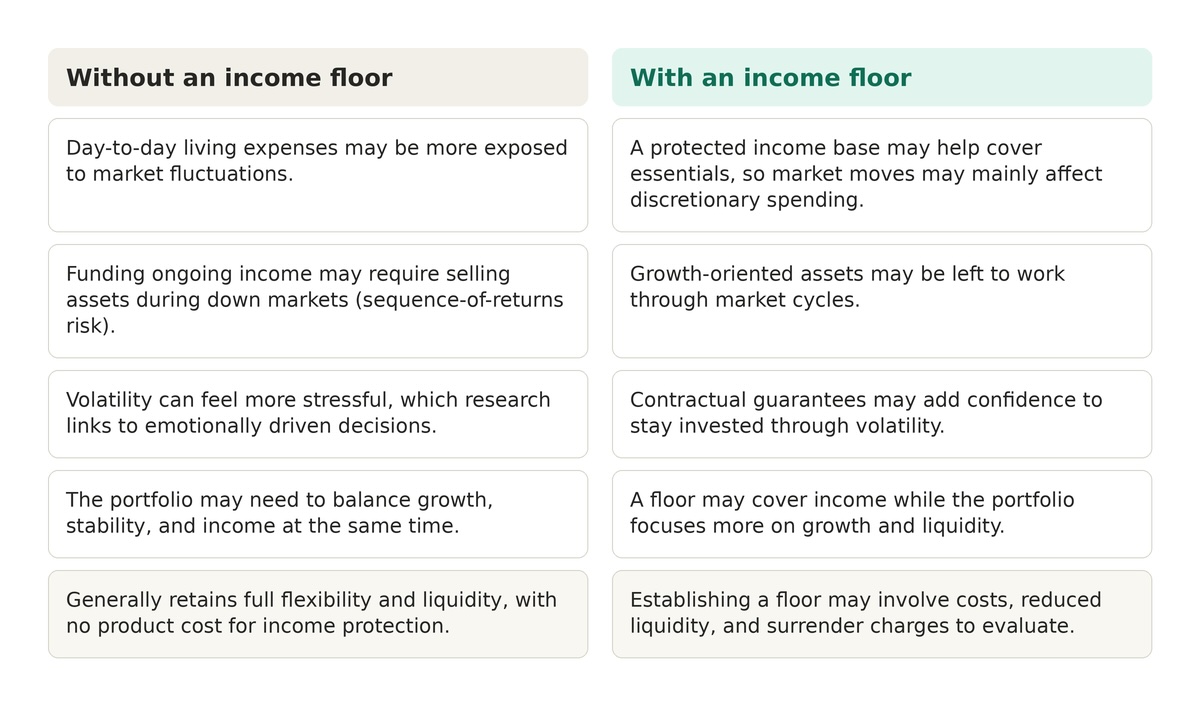

If you are forced to sell equities during a bear market to pay your rent or buy groceries, you lock in losses and permanently deplete your portfolio’s compounding power.

●Traditional Portfolio: Market Crash = Forced Asset Sales =Permanent Capital Loss

●Income Floor Portfolio: Market Crash =Expenses Covered by Guaranteed Income = Equities Left to Recover

When you have a contractual income floor (such as Social Security, a pension, or an annuity) covering your baseline needs, you don’t need to touch your equities during a downturn. Your lifestyle is protected by the floor, and your growth assets are given the time they need to recover. An income floor effectively buys you time, and in investing, time is the ultimate risk-mitigator.

2. Unlocking a Higher "Risk Capacity" for Growth Assets

Paradoxically, securing a conservative income floor can allow you to be more aggressive with the remainder of your portfolio.

In traditional financial planning, as you age, you are told to shift your portfolio into low-yielding, conservative bonds to protect your principal. However, with inflation eating away at purchasing power, a heavy bond allocation can stall your portfolio's growth.

When your essential expenses are contractually guaranteed, the rest of your portfolio transforms into surplus capital. Because you don't rely on these assets for day-to-day survival, you can afford to take more calculated risks. You can maintain a higher allocation to equities, real estate, or other growth-oriented vehicles that outpace inflation over the long term.

3. The Psychological Buffer Against Panic Selling

Market volatility is inevitable, but panic selling is a choice. Most investors underperform the broader market because emotions drive them to sell at the bottom and buy at the top.

An income floor acts as a psychological circuit breaker. When the stock market drops 20%, an investor relying solely on a 4% withdrawal rate from a volatile portfolio feels an immediate threat to their livelihood.

Conversely, an investor with an income floor knows that no matter how bad the headlines get, their mortgage is paid and their groceries are covered. This peace of mind prevents emotional, short-sighted decisions, allowing the volatile portion of the portfolio to do its job without human interference.

4. Redefining the Role of Fixed Income

In a standard portfolio, bonds serve two purposes: generating income and mitigating equity volatility. But in an unpredictable economic environment, relying on them heavily can create a "drag" on your wealth.

When you replace a portion of your fixed-income portfolio with a contractual income base, you free your remaining assets to be used purely for tactical liquidity or opportunistic rebalancing. The floor handles the income, allowing your cash and liquid reserves to act purely as a buffer.

Summary: The Structural Shift

The Bottom Line

An income floor doesn't just add a steady paycheck to your retirement strategy; it changes the chemistry of your entire balance sheet. By contractually securing your downside, you liberate your upside. It transforms volatility from a terrifying threat into a manageable market cycle, stabilizing both your portfolio's returns and your peace of mind.

A Quick Disclosure From Dora:

Hey there! Thanks for reading. Just a quick reminder that while I love talking strategy, this article is for educational and informational purposes only. Every financial situation is unique, and this isn't personal financial, tax, or investment advice. Contractual guarantees are backed strictly by the financial strength and claims-paying ability of the issuing company. Let's look at your specific numbers together before making any big moves! MY Calendar is Here