2026 Retirement Alert: How the "Tax Torpedo" Hits Retirees with $2.5M+ IRAs

For many families reaching a $2.5 million IRA balance is a dream come true. However, under 2026 tax laws, that success can trigger a hidden "wealth tax" that many local retirees don't see coming until they receive their first tax bill in April.

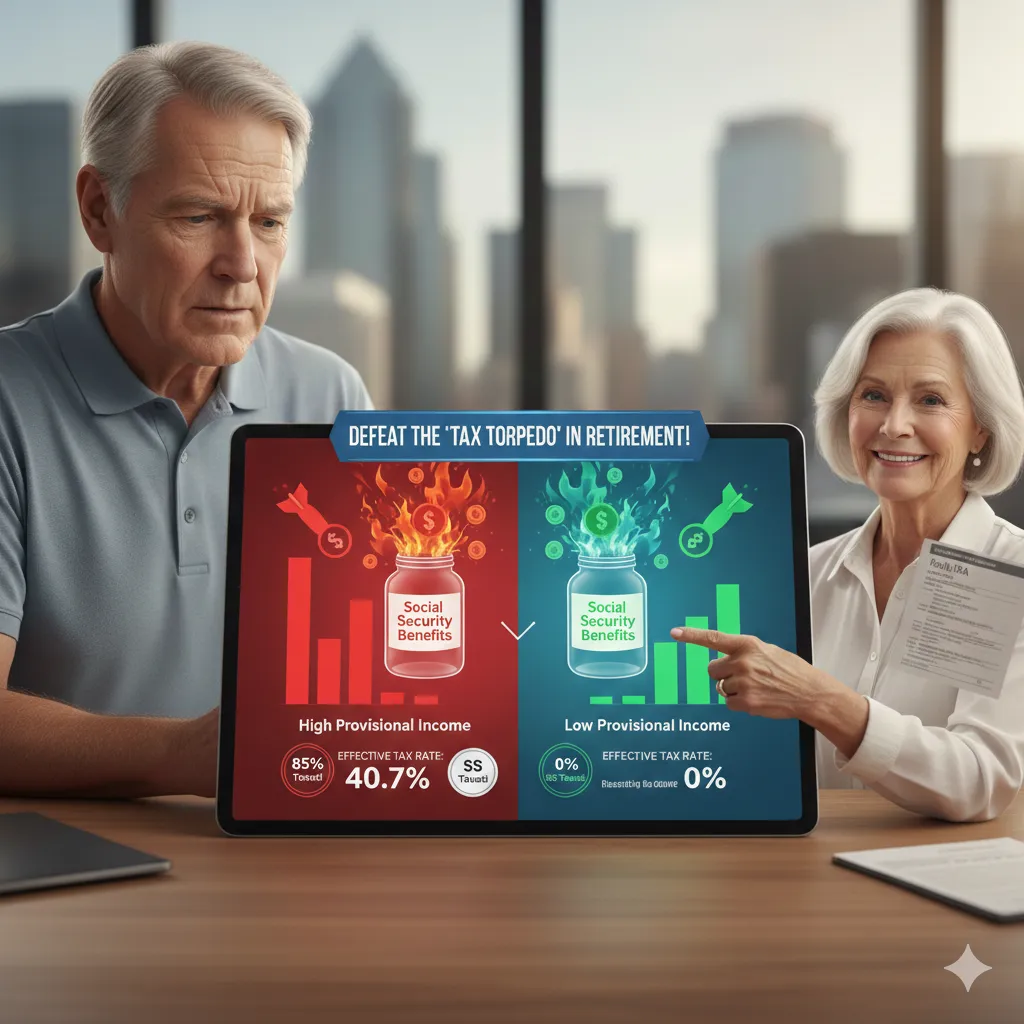

It’s called the Social Security Tax Torpedo. It isn't a hike in your tax bracket; it’s a math trap triggered by Required Minimum Distributions (RMDs) that forces the IRS to tax up to 85% of your Social Security benefits.

Case Study: The $2.5M "Forced Torpedo"

Let’s look at a common scenario we see in our office. Meet Robert and Linda, a retired couple (both age 73) with a successful career history and a combined $2.5M IRA.

Fixed Income: $82,000 (Social Security) + $63,000 (Pensions)

The 2026 RMD: The IRS mandates they withdraw approx. $94,340 this year.

The Problem: Reality A (The Traditional IRA Trap)

Because Robert and Linda hold their savings in a Traditional IRA, the IRS views their RMD as "ordinary income." This creates a domino effect:

Provisional Income Spike: Their "Provisional Income" hits $198,340.

The Torpedo Hits: Because they are over the $44,000 threshold, 85% of their Social Security ($69,700) is now added to their taxable income.

The Invisible Rate: Every $1,000 of RMD effectively taxes them on $1,850 of total income.

2026 Federal Tax Bill: Approx. $34,500

Annual Spendable Cash: $204,840

Effective Rate: $1,850 x 24% tax = $444 tax. That’s a 44.4% effective tax rate on a 24% bracket!

The Solution: Reality B (The Strategic TFRA Alternative)

What if Robert and Linda had worked with a retirement specialist to move those assets into a TFRA (Tax-Free Retirement Account) or Roth environment before age 73?

In this scenario, they still "withdraw" the same $94,340 for their lifestyle, but the tax treatment is fundamentally different:

Zero RMDs: TFRAs under Section 7702 have no mandatory distributions.

The Invisible Income: The $94k is tax-free and—crucially—does not count toward their Social Security taxation formula.

Defusing the Torpedo: Their taxable income is slashed because their Social Security stays largely protected.

2026 Federal Tax Bill: Approx. $12,400

Annual Spendable Cash: $226,940

The Verdict: A $22,100 Annual Bonus

By shifting the "tax bucket" of their assets, Robert and Linda keep an extra $22,100 every single year. That is money they can spend right here in on travel, family, or local legacies rather than sending it to Washington.

Why You Need a Analysis

Tax laws in 2026 are complex, and generic online calculators often miss the nuances of the Tax Torpedo. I am Dora and I specialize in helping high-net-worth families "uncouple" their Social Security from the IRS's aggressive RMD formulas.

Tip: If you are between the ages of 62 and 72, you are in the "Bridge Years." This is the most critical window to defuse the torpedo before it strikes at age 73.

Is your Social Security at risk?

Click below to schedule your custom "Tax Torpedo Analysis." Let’s make sure your $2.5M serves you, not the IRS.