You've Spent Decades Building This. Let's Make Sure the Tax Code, the Market, and Time Work in Your Favor — Not Against It.

Dora Wysocki, CAS® · Certified Annuity Specialist · Certified Tax Specialist (CTS™ — In Progress)

I help pre-retirees build a guaranteed income floor they cannot outlive. I help high earners build a tax-free accumulation strategy their 401(k) alone cannot create. Three coordinated insurance tools. No AUM fees. CPA collaborative. Licensed in 10 states.

You get one retirement. The tools that protect it — and the way they coordinate with each other — matter more than most people realize until it is too late to change course.

CAS® Certified · CTS™ In Progress · Five Risks Coordinated · No AUM Fees · CPA Collaborative · Licensed in 10 States · Google 5★

What happens in the 30-minute analysis? Purely educational. No obligation.

One Specialist, Two Solutions

Two Different Problems. Two Specific Solutions. One Specialist Who

Coordinates Both.

Within 10 Years of Retirement

If you are within 10 years of retirement and concerned about market exposure, outliving your savings, or the tax burden on your 401(k) — you need a guaranteed income floor and a Roth conversion coordination strategy that work together as one plan. The instrument is an annuity. The connection to your CPA is what makes it complete.

Earning $200K or More

If you are earning $200K or more, have maximized your 401(k) contributions, and are still writing a substantial check to the IRS each April — you need a tax-free accumulation vehicle with no IRS contribution limits and no RMDs, coordinated with a Roth conversion strategy designed for your income level. The instrument is IUL. The coordination with your CPA is what makes it complete.

You're Not Behind

If You've Been Meaning to Address This, You're Not Behind. You're at the Right Moment.

Most people who find this page have done the right things. They saved consistently. They worked with a CPA. They invested carefully. What they often haven't had is someone who coordinates all the pieces — the income side, the tax side, and the protection side — as one connected plan.

That is not a failure. It is simply a gap that most financial professionals are not structured to fill. This practice is built specifically for that gap.

The 30-minute Retirement Gap Analysis is purely educational. You'll leave with a clear picture of which of the five retirement risks your current plan addresses well — and which ones it doesn't. No products are sold in that conversation. No obligation follows.

A Note on Fit

This Practice Is Designed for a Specific Type of Client.

Here Is Who It Is Not For

This is not for someone looking for a quick product comparison or a single Annuity or IUl quote.

This is not for someone who is not yet serious about coordinating their retirement income plan, their tax picture, and their protection strategy as one connected system.

This is not for someone who has no interest in working collaboratively with their CPA as part of the planning process.

If that is you — there are many excellent resources available, and we respect that entirely the general approach to retirement.

This practice works with pre-retirees, retirees, and high earners who are ready to think about retirement income as an engineered system — and who want a specialist who coordinates the insurance products architecture like Annuities or IUL, hands their CPA a complete picture, and charges no ongoing AUM fee for doing so.

If that description fits — the Retirement Gap Analysis is a good first step.

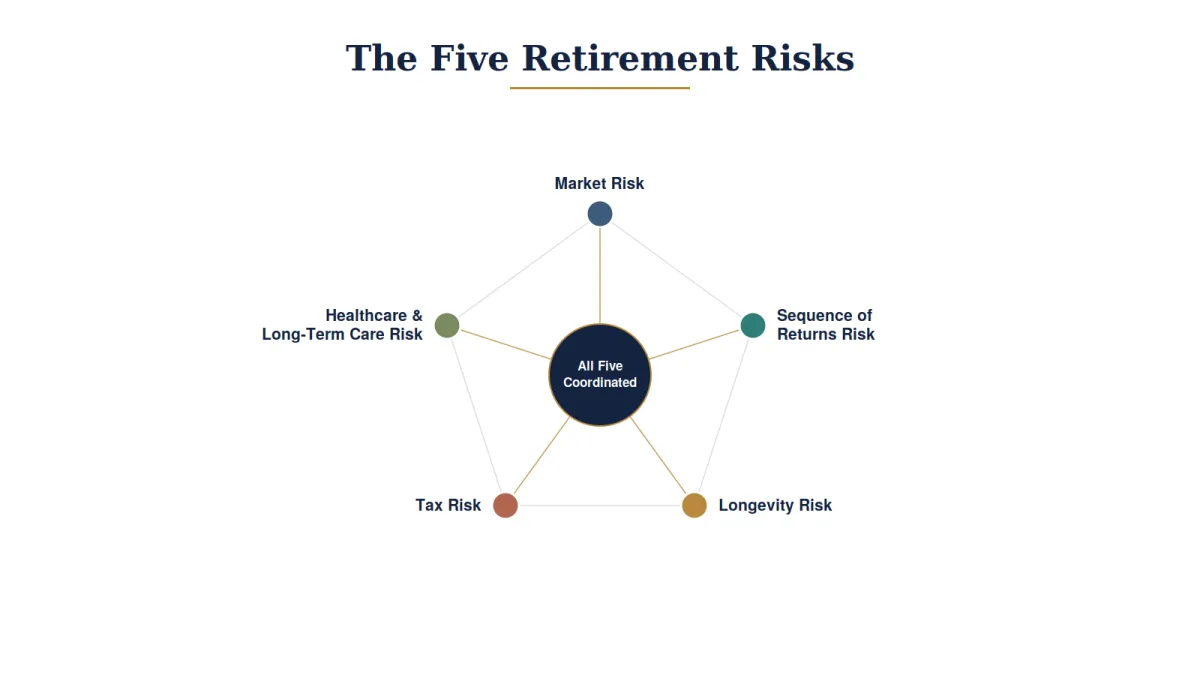

Five Retirement Risks

The Five Retirement Risks. Most Advisors Address One.

This Practice Coordinates All Five.

Market Risk &

Sequence of Returns

A 20% market loss in year one of retirement can cause four times more cumulative damage than the same loss fifteen years in. A Fixed Index Annuity addresses this structurally: your income floor is established by contract, and downward index movement results in a zero indexed credit — not a negative one.

Annual insurance charges apply. Guarantees are backed solely by the claims-paying ability of the issuing insurance company.

Longevity Risk &

Tax Risk

The average retirement lasts 25 to 30 years; most plans are designed for 15. Every dollar in a traditional 401(k) comes out taxed as ordinary income, and RMDs at age 73 force withdrawals whether you need them or not. A contractual income floor plus a coordinated Roth conversion strategy — executed with your CPA — can address both.

Healthcare &

Long-Term Care Risk

Private nursing home care now exceeds $100,000 per year, and 70% of people turning 65 will need some form of care. Hybrid Life and LTC solutions offer a two-outcome structure: if care is needed, the benefit pool is available tax-free; if not, a tax-free death benefit passes to your family.

Guarantees are backed solely by the claims-paying ability of the issuing insurance company.

60-Second Self-Assessment

What Is Your Biggest Retirement Gap? — 60 Seconds to Find Out

FOR HIGH EARNERS

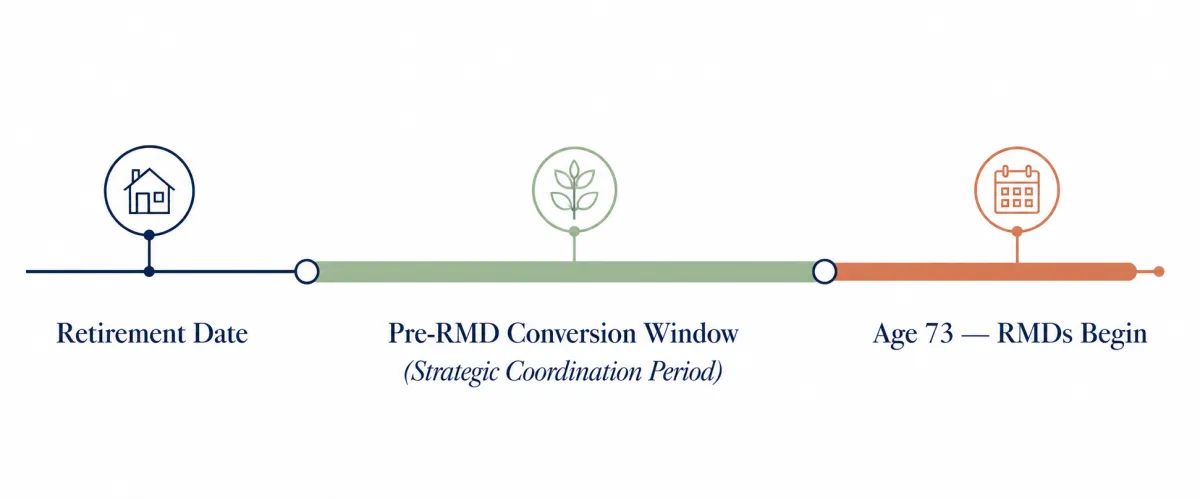

The Conversion Window. Most High Earners Don't Know It Exists. Fewer Know How to Use It.

Between the day you stop working and the day Required Minimum Distributions begin at age 73, there is a window. Your income is lower. Your effective tax bracket is lower. Annual Roth conversion capacity exists — the precise amount depends on your filing status, all income sources, and current tax brackets. Every year that window goes unused is permanently gone

The role of this practice: identify the window, model how it interacts with your annuity income floor and IUL strategy, and deliver a complete coordination picture to your CPA. Your CPA determines the optimal annual conversion amount, manages IRMAA Medicare premium thresholds, and executes the filing. Both sides work as one system.

CLIENT REVIEWS

What Clients Say on Google

DW Financial Group · (908) 738-9836